A patient hands over an insurance card. It says ‘Medicare’ on it. The staff member assumes standard Medicare rules apply, checks basic eligibility, and sends the patient back. Fast forward two weeks, and the claim comes back denied — because the patient is actually enrolled in a Medicare Advantage plan with a completely different network, prior authorization requirement, and reimbursement structure.

This is one of the most common and costly billing mistakes in healthcare today. Medicare is not one thing anymore. There are two fundamentally different Medicare pathways that your patients can be on, and understanding the difference between them is not optional for providers who want to get paid correctly, avoid compliance issues, and deliver a smooth patient experience.

As of 2024, more than 33 million Medicare beneficiaries — that is, roughly 54% of all Medicare enrollees — are now enrolled in Medicare Advantage plans, according to the Kaiser Family Foundation. That means more than half of your Medicare patients are not on Original Medicare. They are on private plans that look like Medicare but operate by entirely different rules. This guide explains those differences clearly, from a billing and compliance standpoint.

What Is Original Medicare?

Original Medicare is a government-administered health insurance program managed by the Centers for Medicare & Medicaid Services (CMS) that pays providers directly based on a standardized fee schedule.

What Is Medicare Advantage?

Medicare Advantage is a Medicare-approved plan offered by private insurance companies that replaces Original Medicare and manages claims, networks, and reimbursement rules.

Original Medicare: How It Actually Works

Original Medicare, also called Traditional Medicare or Fee-for-Service Medicare, is the government-administered health insurance program established in 1965. It is run directly by the Centers for Medicare and Medicaid Services (CMS) and covers two main parts.

Medicare Part A

Part A covers inpatient hospital care, skilled nursing facility stays, hospice care, and some home health services. Most beneficiaries receive Part A premium-free if they or their spouse paid Medicare taxes during working years. The hospital inpatient benefit is subject to a benefit period deductible, which is $1,632 in 2024, with coinsurance kicking in after 60 days of inpatient care.

Medicare Part B

Part B covers outpatient services, physician services, preventive care, durable medical equipment, and certain home health services. Beneficiaries pay a monthly premium — $174.70 in 2024 for most enrollees — plus a $240 annual deductible, and then 20% coinsurance after the deductible is met.

How Providers Bill Original Medicare

This is the part that matters most for your billing team. Under Original Medicare, you submit claims directly to CMS through a Medicare Administrative Contractor (MAC) assigned to your geographic region. You bill using standard CPT and ICD-10 codes, and Medicare pays according to the national fee schedule — either the Medicare Physician Fee Schedule for professional services or the Hospital Outpatient Prospective Payment System for outpatient facilities.

One of the biggest advantages of Original Medicare for providers is predictability. The fee schedule rates are published annually by CMS. You know exactly what Medicare will pay for a given code, and you know which codes require prior authorization and which do not. There are fewer surprises on the back end.

Original Medicare also has no provider network. Any provider who accepts Medicare assignment can see any Medicare beneficiary. You do not need to be credentialed with a specific plan or worry about network adequacy. A patient with Original Medicare can walk into any Medicare-enrolled practice in the country.

Medicare Advantage

Medicare Advantage — officially called Medicare Part C — is an alternative way for Medicare beneficiaries to receive their Medicare benefits through a private insurance company that contracts with CMS. Instead of CMS paying claims directly, CMS pays the private insurer a capitated monthly amount for each enrolled beneficiary, and the insurer takes over the administration of that patient’s Medicare benefits.

Medicare Advantage plans are required by law to cover everything that Original Medicare covers. But the similarity mostly ends there. The way these benefits are structured, delivered, and paid for is fundamentally different — and those differences directly affect how you practice and how you bill.

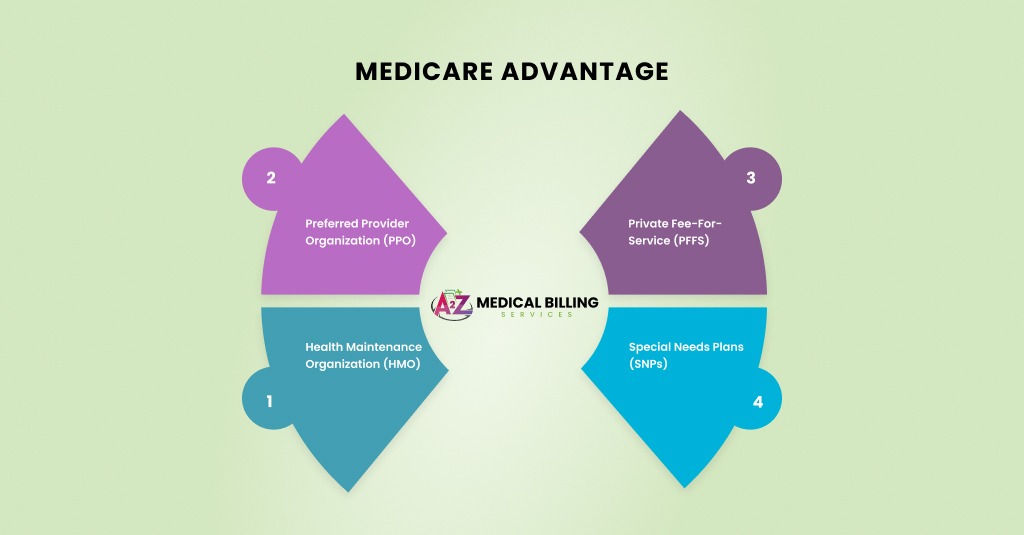

Medicare Advantage Plan Types

Not all Medicare Advantage plans are structured the same way. Understanding the plan type your patient is enrolled in matters because it determines network rules and referral requirements.

- Health Maintenance Organization (HMO): The most restrictive structure. Patients must use in-network providers except in emergencies. They are usually assigned to a Primary Care Physician who coordinates all care. Specialist visits typically require a referral. As a specialist or ancillary provider, if you are not in-network for an HMO plan, you generally cannot see that patient at all except in emergencies.

- Preferred Provider Organization (PPO): More flexible. Patients can see out-of-network providers but pay more to do so. In-network providers are reimbursed at a negotiated rate; out-of-network providers may be reimbursed at a lower rate or the patient faces significantly higher cost-sharing.

- Private Fee-for-Service (PFFS): The insurer sets its own payment rates. Providers who agree to the plan’s terms can see these patients. Unlike HMO plans, most PFFS plans do not require a network contract.

- Special Needs Plans (SNPs): Designed for beneficiaries with chronic conditions, dual Medicare/Medicaid eligibility, or those in institutions. These plans have the most specialized coverage structures and often the most restrictive network and PA requirements.

Side-by-Side Comparison: Original Medicare vs. Medicare Advantage

| Feature | Original Medicare | Medicare Advantage |

| Administered by | Federal government (CMS) | Private insurance companies |

| Provider network | Any Medicare-enrolled provider nationwide | Network-restricted (HMO/PPO) |

| Referrals | Not required for specialists | Often required (especially HMO) |

| Prior Authorization | Limited — mainly for certain services | Extensive PA requirements |

| Prescription Drugs | Separate Part D plan needed | Usually included (MAPD) |

| Extra benefits | None beyond Parts A/B | Dental, vision, hearing, gym |

| Claims filed by | Provider bills CMS directly | Provider bills the plan |

| Out-of-pocket max | None (unlimited exposure) | Annual cap required by law |

| Billing rules | CMS national fee schedule | Plan-specific contracted rates |

Key Questions Providers Ask About Medicare Advantage vs Original Medicare

Can you bill Medicare Advantage the same way as Original Medicare?

No. Medicare Advantage claims are submitted to private insurers, not directly to Medicare, and each plan has its own rules.

Do Medicare Advantage plans require prior authorization?

Yes. Most Medicare Advantage plans require prior authorization for many services, unlike Original Medicare, which has limited requirements.

Why are Medicare Advantage claims denied more often?

Denials often occur due to missing prior authorization, incorrect network usage, or plan-specific billing rules.

Prior Authorization: The Biggest Operational Difference

If there is one difference between Original Medicare and Medicare Advantage that causes the most friction for providers, it is prior authorization. And the data backs this up.

A 2023 report from the American Medical Association found that 94% of physicians reported that prior authorization delays care, and 89% said it negatively impacts patient outcomes. Much of this burden falls on Medicare Advantage patients. According to a 2023 OIG report, Medicare Advantage plans denied 13.6% of prior authorization requests in 2021, and many of those denials were later overturned on appeal — suggesting that a significant number of initially denied services were medically appropriate.

Under Original Medicare, prior authorization requirements are relatively limited. CMS requires prior authorization for certain high-cost imaging services and some outpatient hospital procedures, but the list is much shorter than what most Medicare Advantage plans require. Under Medicare Advantage, virtually any service — from imaging to surgical procedures to post-acute care placements — can require prior authorization, and the requirements vary by plan.

For your practice, this means your staff needs to verify PA requirements separately for each Medicare Advantage plan. What United Healthcare requires for a knee MRI may be completely different from what Humana requires or what Aetna Medicare Advantage requires. There is no single reference for all Medicare Advantage PA requirements. You need to check each plan’s portal or call the plan’s provider services line. Providers should also understand how Advance Beneficiary Notices (ABNs) apply when services may not be covered under Medicare.

The consequences of missing a required PA under Medicare Advantage are serious. Unlike Original Medicare, where you might have grounds for a retrospective appeal based on medical necessity documentation, most Medicare Advantage plans will deny a claim outright for missing prior authorization with no path to retroactive approval.

Quick Summary: Key Differences That Impact Billing

- Medicare Advantage requires prior authorization for many services

- Original Medicare has standardized billing rules

- Medicare Advantage plans have network restrictions

- Reimbursement rates vary by plan under Medicare Advantage

- Timely filing limits differ across plans

Billing and Reimbursement Differences

From a pure billing standpoint, Original Medicare and Medicare Advantage are two separate worlds. Here is what your billing team needs to understand about each. These billing differences are closely tied to denial management and overall revenue cycle performance, making it essential to have a structured billing process in place.

Billing Original Medicare

Claims go to your MAC using the standard 837P (professional) or 837I (institutional) electronic claim format. You use the patient’s Medicare Beneficiary Identifier (MBI) number from their red, white, and blue Medicare card. Payment is based on the Medicare Physician Fee Schedule or applicable prospective payment system. Timely filing limits are 12 months from the date of service.

Billing Medicare Advantage

Claims go to the private insurer, not to CMS. You use the member ID from the Medicare Advantage insurance card — not the red, white, and blue Medicare card number. Timely filing limits vary by plan and are often shorter than Medicare’s 12-month window. Some plans require 90 days, others 180 days. Missing the timely filing deadline under a Medicare Advantage plan is grounds for denial with limited appeal rights.

Reimbursement rates under Medicare Advantage also vary by plan. Some plans pay above Medicare fee schedule

rates to attract strong provider networks. Others pay at or below Medicare rates. Since you negotiate these rates directly with each plan, or accept their standard terms when you sign a network agreement, you should be regularly reviewing your Medicare Advantage contracts to ensure you understand what you are being paid for each service.

Medicare Billing Workflow: Original Medicare vs Medicare Advantage

Understanding the billing workflow difference helps reduce errors and delays.

Original Medicare Workflow:

- Verify Medicare eligibility

- Provide services

- Submit claim to MAC

- Receive payment based on the fee schedule

Medicare Advantage Workflow:

- Verify plan type and network status

- Check prior authorization requirements

- Provide services

- Submit claim to insurance plan

- Follow up on denials or additional documentation

Coordination of Benefits Under Medicare Advantage

When a Medicare Advantage patient has secondary insurance — such as a Medigap supplement or employer retiree coverage — the COB rules are more complex. Medigap plans, for example, are not designed to work alongside Medicare Advantage plans. Patients who switch from Original Medicare to a Medicare Advantage plan typically lose their Medigap coverage benefits. This is a common source of patient confusion that ends up in your billing department.

What Attracts Patients to Medicare Advantage

One reason Medicare Advantage enrollment has grown so dramatically is the extra benefits these plans offer that Original Medicare does not cover. Understanding these benefits helps you understand your patient population and anticipate their expectations.

Medicare Advantage plans are permitted — and often incentivized by CMS — to offer supplemental benefits beyond what Original Medicare covers. These can include:

- Routine dental care, including cleanings, X-rays, and some restorative work

- Routine vision care, including eye exams and allowances for glasses or contacts

- Hearing aids and hearing exams

- Over-the-counter allowances for health-related products

- Transportation benefits for medical appointments

- Fitness memberships such as SilverSneakers

- Telehealth services beyond what Original Medicare covers

These extra benefits create both an opportunity and a complexity for providers. On one hand, patients with Medicare Advantage dental or vision benefits may seek more preventive care. On the other hand, the structure of these supplemental benefits varies enormously by plan, and patients often overestimate what is covered. Managing those expectations is part of good patient financial communication.

Why Medicare Advantage Billing Requires Specialized Expertise

Managing Medicare Advantage billing requires more than basic Medicare knowledge. Each plan has its own rules for prior authorization, reimbursement, and claim submission.

For many practices, handling these complexities internally can lead to increased denials, delayed payments, and administrative burden. Working with an experienced medical billing team can help ensure compliance, reduce errors, and improve revenue cycle performance.

Best Practices for Your Practice Operations

If your practice sees a significant number of Medicare patients — and most do — your operations need to account for the fact that your Medicare patients are no longer a homogenous group. They fall into at least two distinct categories with different rules, different billing paths, and different authorization requirements.

Here are the operational implications to build into your workflow:

- Train your front desk to distinguish between Original Medicare and Medicare Advantage cards. The red, white, and blue card signals Original Medicare. Any other card branded with an insurer name — Humana, United, Aetna, Cigna, Blue Cross — that also says Medicare on it is likely a Medicare Advantage plan.

- Verify benefits separately for every Medicare Advantage plan. Do not assume that what one plan covers, another plan will too. Check each plan’s specific benefits and PA requirements at every visit.

- Know your network status with each Medicare Advantage plan. Being enrolled in Medicare does not mean you are in-network with every Medicare Advantage plan. You need to be specifically credentialed with each plan’s network. If you are out-of-network, understand what that means for your patients’ cost-sharing.

- Track timely filing deadlines separately for each plan. Medicare Advantage timely filing windows vary. Build plan-specific timely filing calendars into your denial management process.

- Audit your Medicare Advantage contracts regularly. Reimbursement rates, PA requirements, and covered services under Medicare Advantage plans can change annually. Review each contract at renewal time.

Final Takeaway for Providers

Original Medicare offers predictable billing and fewer administrative barriers, while Medicare Advantage introduces plan-specific rules, prior authorization requirements, and variable reimbursement structures.

Understanding these differences is critical to reducing denials, improving cash flow, and maintaining a smooth billing workflow.

Final Thoughts

The distinction between Original Medicare and Medicare Advantage is no longer a niche topic for large hospital billing departments. It is a daily operational reality for every practice that treats Medicare-age patients — which is essentially every practice in the United States.

As Medicare Advantage enrollment continues to grow, the complexity this creates for providers will only increase. More plans, more plan-specific rules, more prior authorization requirements, and more variation in reimbursement rates. The practices that navigate this landscape successfully are the ones that build these distinctions into their eligibility verification workflows, their billing processes, and their staff training from day one.

Know which Medicare your patient is on before the encounter. Verify benefits specifically for that plan. Check PA requirements before delivering services. Know your network status. Track your timely filing deadlines. And review your Medicare Advantage contracts regularly to make sure you are being paid fairly for the care you deliver.

The administrative complexity of Medicare Advantage is real — but so is the revenue opportunity. Over 33 million Americans are on these plans and that number is growing every year. Mastering the operational differences between Original Medicare and Medicare Advantage is one of the most practical steps your practice can take to protect revenue and reduce denials in today’s environment.